RA or employer fund?

The bad news is that, unless you receive a large inheritance or win the Lotto, we all need to save up for our later years. The good news is that you can now allocate up to 27.5% of your total annual income to a retirement fund and pay less tax. Even if you’re not able to make the maximum tax-deductible contribution, every hundred rand that you can set aside for retirement is a heroic act of taking care of your future self, considering the financial squeeze South Africans are currently experiencing.

For the self-employed, a retirement annuity (RA) is the go-to solution for reducing the amount of annual income on which you need to pay provisional and final assessed tax every year – and it builds financial reserves for those later years (after age 55) in which you may want to reduce your working hours or simply take a break. In addition, it provides a safety net in case you are ever liquidated; creditors are not allowed to touch the money saved up in an RA, while it’s in the fund.

For employees, both their employer’s retirement fund and an RA provide all the benefits above, making it difficult to choose between the two options. But what exactly is the difference between contributing more to your employer’s fund and topping up your RA?

The timing of your contribution and tax ‘refund’

With an RA, employees will only be rewarded with a tax refund (provided you don’t have sources of income other than your salary) for any RA top-ups during a particular tax year after you’ve filed your tax return and SARS has completed the assessment for that tax year.

If you want to add money to your employer’s fund, you normally need to commit to the increased contribution for a year and many companies will only allow you to change the monthly contribution amount on a fixed date every year. You don’t have the flexibility to simply top-up your employer’s fund on an ad hoc basis. You therefore need to make sure that you’ll be able to afford the higher amount for an entire year. On the upside, this enforces the discipline of living off a smaller net salary so your savings can grow faster.

Also, importantly, with employer fund contributions the tax relief is immediate from the day you increase your contribution – you don’t need to wait for a tax refund later in the year. Your payroll administrator will re-calculate your taxable income and you’ll see a lower tax amount on your payslip. For example, if you’re in the 36% tax bracket, an additional R1000 monthly contribution to your employer’s fund will lead to only R640 less in your bank account. You’ll save R360 per month in tax straight away, while your life savings are growing by R1 000 more per month. Put differently, SARS is giving you R360 to save R1 000 more every month for yourself.

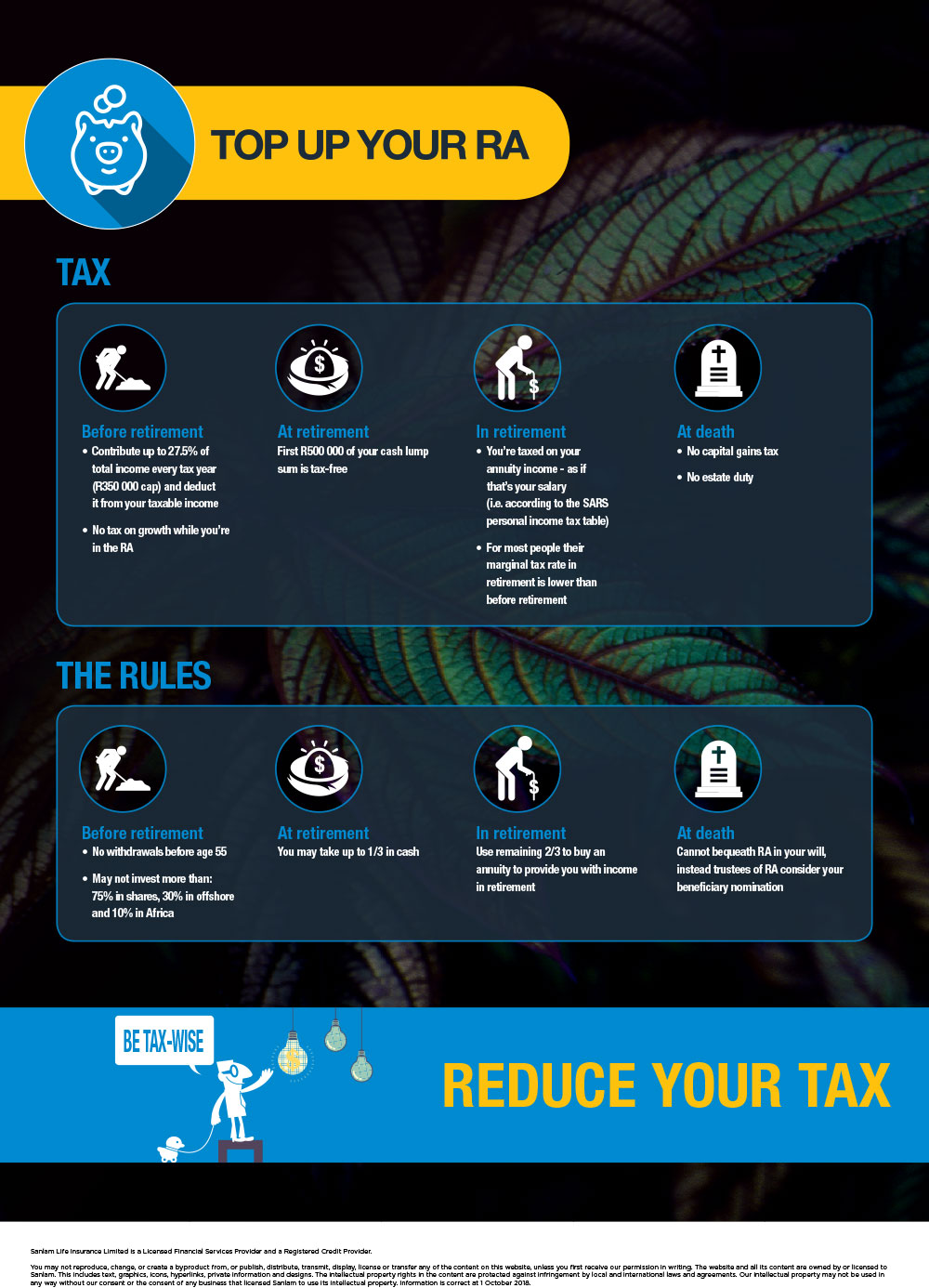

View our RA refund infographic to see more examples of how much tax you can save this 2021/22 tax year if you contribute to an RA.

We’ve also created an infographic to give a summary of the main rules and tax treatment of an RA at a quick glance.

The amount of cash you may take when you retire

If your employer’s fund is registered as a pension fund, there is no difference in the treatment of your RA money and your share of your employer’s fund at your retirement date. But if the employer’s fund is registered as a provident fund, things work a bit differently.

For both an RA and a pension fund you may take up to one-third of the value of your savings in cash, of which the first R500 000 across all your retirement products can be taken tax free. With the remaining two-thirds you need to buy an annuity income, which is taxable.

With a provident fund, you used to be able to take all of your savings in cash; there was no obligation to buy an annuity income. But since 1 March 2021 a provident fund is treated the same as an RA and a pension fund. Your contributions before this date will be ring-fenced and the old rules still apply to this portion. But for any contributions after this date, and the growth on these contributions, the rules work the same as for an RA and a pension fund: on retirement you need to buy an annuity with the remaining two-thirds after taking your cash portion.

It boils down to cash flow and timing

To summarise, faced with the choice between adding more to either your RA or your employer’s fund, it boils down to your cash flow circumstances. If you can commit to a monthly contribution increase, your employer’s fund offers immediate tax relief. But if you’re concerned that you might run into a cash flow pinch with the resultant lower net salary, an RA might be a better idea – giving you the flexibility to contribute only when you can afford it. Either way, you’re taking a positive step towards creating more financial freedom for yourself in future. Hats off to you.

Share On:

Comments are closed.