The lost decade of the JSE: SA small- and mid-cap shares

by Vanessa van Vuuren, portfolio manager at Sanlam Investments

The small-cap premium – fact or fiction? Since Eugene Fama and Kenneth French first published their US-focussed research around the so-called “size” or “small-cap premium” in 1992, debate has ebbed and flowed around whether this premium does in fact exist. In theory, the notion of a higher return to be extracted from smaller shares makes sense. These companies are growing and evolving faster than their established and mature counterparts, and they tend to have less liquidity, with limited published investment research available, potentially resulting in greater mis-pricings of what these companies are potentially worth.

Closer to home, a simple long-term cumulative return analysis of the JSE broken down into the Top 40, mid-cap and small-cap indices over a 30-year period seems to suggest clear evidence for the outperformance of mid and small caps relative to their larger Top 40 counterparts over this long-term horizon.

There are, however, two key elements to consider, and which we added to our analysis:

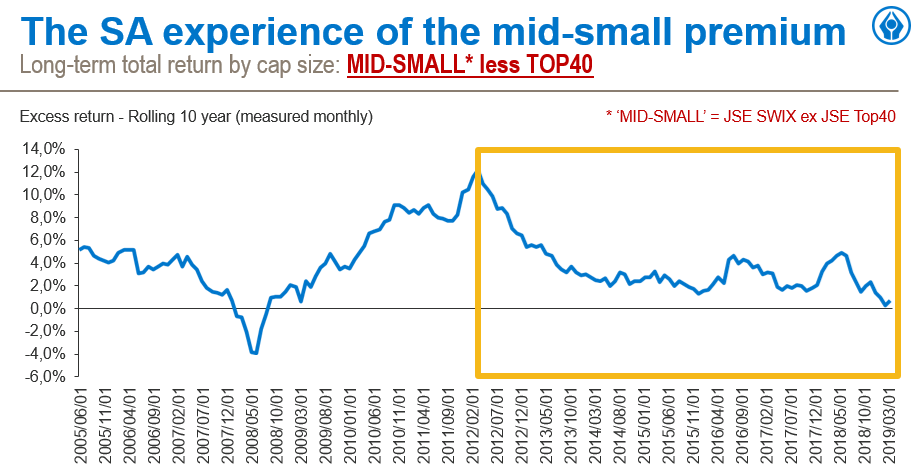

1) The starting point matters. The premium to be extracted from investing in mid and small caps clearly depends on the starting point. The chart below shows the excess return an investor would have generated over a 10-year holding period (which we consider to be a long-term investment horizon) commencing from as far back as 1995. Each point represents rolling monthly data of the 10-year annualised differential in performance between mid- and small-cap shares (represented by the FTSE/JSE Swix ex Top40; earlier the FTSE/JSE All Share ex Top40) and large-cap shares (represented by the FTSE/JSE Top40 Index). The data depicts how the cap size premium return on this rolling ten-year basis has been positive most of the time, but has diminished materially more recently. The latest data point, capturing the last decade, indicates that there has been no cap size premium at all extracted from investing in mid- and small-cap shares.

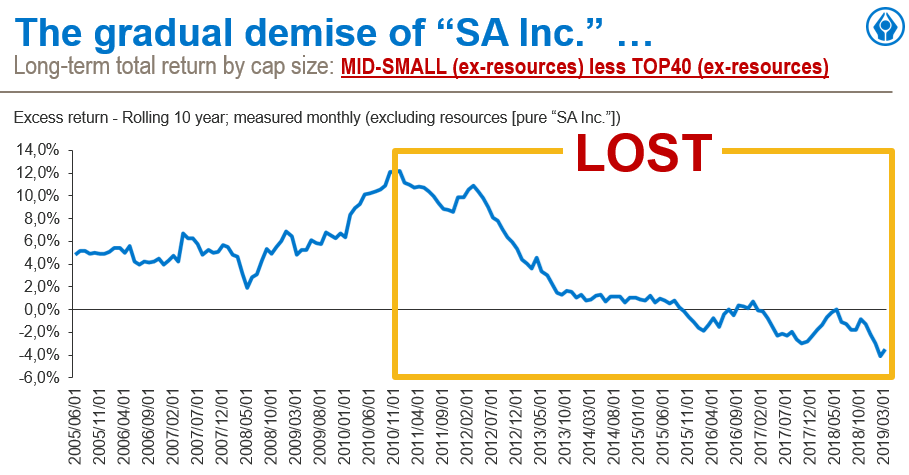

2) The make-up of the underlying index matters. We wanted to ascertain what the performance of the “South African-orientated” mid- and small-cap shares has been and we found that this was best achieved by removing the resource shares from both the mid- and small-cap universe, as well as the large-cap universe, given that the performance of resource shares tends to be a function of global macro drivers, as opposed to local economic dynamics. We then compared the rolling ten-year return differential on that basis and found that the underperformance of domestically focused SA mid- and small-cap financial and industrial shares was even more pronounced versus the Top40 financial and industrial shares, with this differential actually in unprecedented negative territory for the past rolling decade (-4%)! To some extent, the dominance and rise of Naspers and other large dual-listed, rand-hedge Top40 industrial shares has exacerbated this “cap-size” underperformance, but what this essentially tells you is that being invested in SA-focused small- and mid-cap shares over the past ten years has delivered the worst investment performance from the JSE investment opportunity set.

What has driven small and mid caps’ underperformance?

In the decade following the financial crisis, a myriad of issues circling the local economic and political landscape caused companies depending on domestic demand to face serious headwinds. Relative to the Top 40 financial and industrial (FINDI) universe, the mid- and small-cap FINDI stocks are, in general, more domestically exposed businesses, deriving a larger portion of their revenues and profits from within South Africa. While key global economies like the US and China have seen strong growth environments over the past decade, allowing corporates to thrive and grow profits, the reality in South Africa stood in stark contrast; we’ve had negligible to zero real economic growth over the past decade. In addition, the gravity of political malfeasance over the same period is only now being fully understood and has created a tangible structural headwind for domestic businesses. This backdrop has fostered a growing negativity around these so called “SA Inc.” stocks and negative sentiment has been exacerbated by the increased frequency of companies reporting results below consensus expectations in the past few years.

Company-specific factors have aggravated investor panic, with multiple corporate failures due to fraud and mismanagement (think ABIL, Steinhoff, EOH, Tongaat), weak business models (companies who grow by acquisitive growth) and over-indebted companies with unsustainable balance sheets becoming vulnerable in a structurally low-growth environment (think Aspen, Ascendis Health, Tongaat and more recently Omnia). Even companies which were widely considered resilient and dependable Top 40 stalwarts, such as Mr Price, AVI and Shoprite, have seen their share prices under significant pressure when reporting unexpected, disappointing operational updates. Moving down the size curve on the JSE, the earnings reports (and subsequent price movements), although less widely publicised, have made for even more dreary reading over the past few years, with some industries, such as the construction sector, literally being wiped out after a decade of this brutal operating environment. (Group Five, Basil Read and Esor all filed for business rescue, with Aveng teetering on the brink.)

So, where to from here?

The relative underperformance of the mid- and small-cap financial and industrial stocks has created a significant buying opportunity in a beaten down sector. In fact, at Sanlam Investments our internal assessment of the potential upside in the mid- and small-cap sector is the highest we have seen in a decade. Admittedly, the local economic backdrop remains challenging. However, taking a longer-term view and analysing the unique drivers of value for businesses from a bottom-up and “through the cycle basis” allows us to look through short-term economic headwinds when assessing investment opportunities for our clients. While the new political leaders have their work cut out for them, they are making all the right structural changes to hopefully rectify the fiscal and policy framework of the SA economy, which further bodes well for setting the stage for an economic recovery.

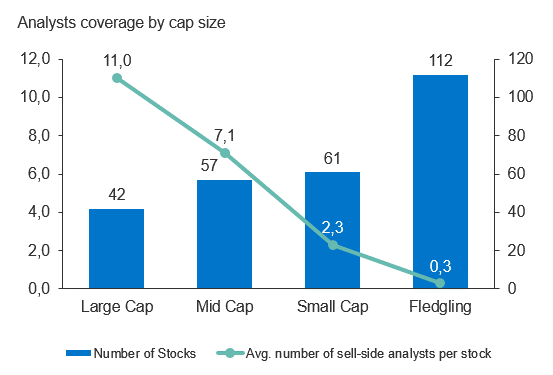

Linking back to the theoretical arguments around the small-cap premium, the level of mispricing we see in the market can perhaps also be attributed to the lack of coverage by the sell-side analyst community in the mid- and small-cap area of the market relative to the Top 40. On average, companies in the Top 40 Index have 11 analysts covering each company while that number drops to 7.1 and 2.3 analysts per company in the mid- and small-cap sectors respectively. The lack of detailed research and coverage creates more price discovery opportunities.

Source: Bloomberg

We believe that for the patient investor, with the means to adequately cover and research the bottom end of the market to uncover hidden gems (and avoid landmines), this “lost decade” of the SA Inc mid- and small-cap universe has created an exceptionally attractive entry point.

Share On:

Comments are closed.