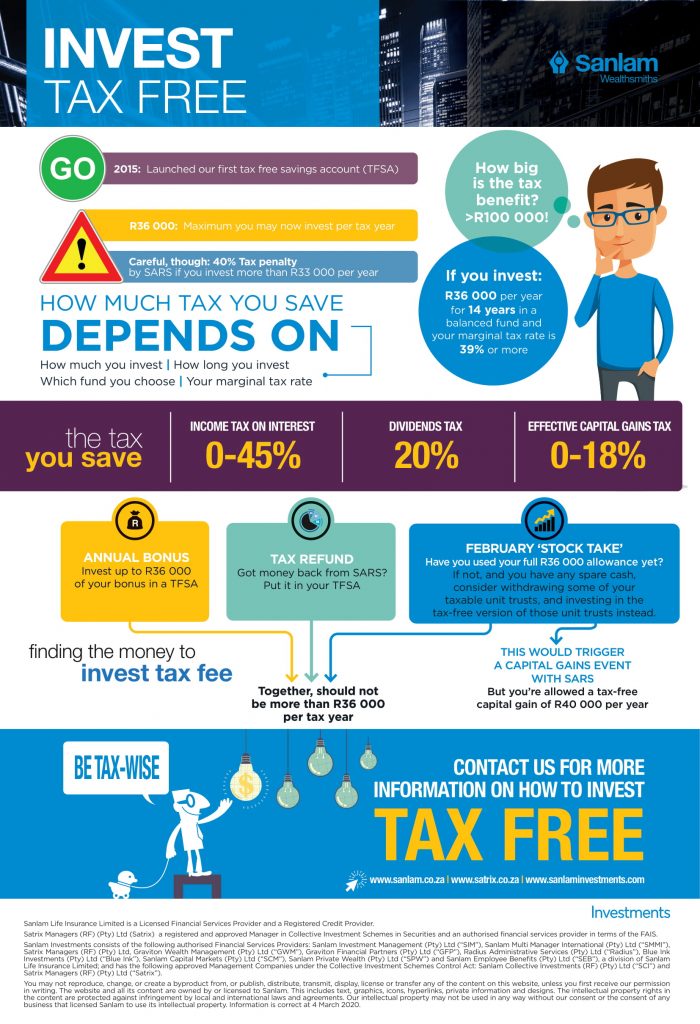

Tax-free saving: everything you need to know

With the end of the tax year fast approaching, you have only until the end of February to top up all the investments that give you that much needed tax break and make use of this year’s allowances. The first type of investment, the retirement annuity (RA), has been around for many years and most investors are familiar with this product. The second type of product, the tax-free savings account (TFSA), was only introduced in 2015, but is fast gaining popularity among retail investors – for obvious reasons.

The benefits of a TFSA

All the proceeds – dividends, interest and capital gains – are tax-free. After several years of investing in a balanced or equity portfolio, the capital gain payable when ultimately withdrawing the money could be substantial. This tax benefit makes the TFSA very attractive relative to discretionary, taxable products.

The contribution limits of a TFSA

Your overall TFSA contributions are limited to R36 000 per tax year. Any contributions exceeding the annual cap will be taxed at 40% and therefore need to be monitored carefully to remain within the annual limit. You cannot roll over this year’s unused allowance to next year, so if you don’t contribute before the end of February, you’ve missed the boat for the tax year. A lifetime contribution limit of R500 000 also applies.

The tax benefits are significant compared to a taxable product

The benefit may be small during the first few years, but as the value of the investment grows, it becomes significant. The difference between investing R2 750 per month in a balanced portfolio TFSA earning 10% p.a. and investing the same amount in a ‘normal’ taxable product earning 10% p.a. before tax over a period of 25 years could result in several hundred thousand rand more in your pocket at the end of 25 years. (In our calculations, contributions cease after 15 years as the lifetime limit is reached, but the money remains invested for the remainder of the 25-year investment period).

The tax benefit of the TFSA is therefore significant for long-term investments that are not invested mainly in cash, but in a balanced portfolio with shares, property and some interest-yielding assets.

What about withdrawals?

Because contributions to a tax-free savings account will be with after-tax money, withdrawals will be tax-free. You may withdraw money at any time, but legislation discourages unnecessary withdrawals: no amount withdrawn may be replaced. Every contribution counts towards the annual allowance and brings you closer to the limit, even if you’re only replacing money withdrawn in that same year.

For example, if you invested R20 000 and then withdrew that R20 000 in the same tax year, you would only be able to contribute an additional R13 000 in the same tax year before reaching the R36 000 annual contribution limit.

How does a tax-free savings account compare with an RA?

A great benefit of both a tax-free investment account and a retirement annuity (RA) is that all the growth and income of the investment are tax-free. This includes tax on interest, dividends and capital growth. However, with an RA, the moment you start to withdraw a retirement income, that annuity income becomes taxable at your personal income tax rate. In contrast, withdrawals from a tax-free investment are not taxable. On the other hand, RA contributions are tax-deductible up to 27.5% of your total income (salary plus other income) for the tax year, while contributions to a tax-free savings account are not tax-deductible.

Both products have their own benefits and should not be seen as competing with one another, but as complementary components of a holistic financial plan. It’s always a good idea to seek sound financial advice before deciding how much to allocate to each product.

Which TFSA products does Sanlam Investments offer?

Sanlam Investments offers 3 tax-free products. They are the:

- Sanlam Collective Investments tax-free unit trusts

- Satrix tax-free unit trusts

- Satrix tax-free ETF range.

The Sanlam Collective Investments tax-free unit trust is for investors who prefer actively managed funds, run by portfolio managers who research and analyse the investment universe before picking only certain assets within an index. The Satrix tax-free unit trust is for those who prefer low-cost index-tracking investments (the portfolio manager buys all the assets in a particular index) and the minimum investment amount is R500 per month.

The anniversary of the first tax-free unit trusts launched in 2015 is coming up and you’ll be pleasantly surprised at the superior annual returns compared to their standard, taxable counterparts, particularly for pure equity and high equity funds. Not paying any dividends tax now and no capital gains tax in future will make a dramatic difference to your pocket. So, make sure to not miss another tax year for planting the seeds for a tax-free harvest in future.

Share On:

Comments are closed.