Risk and volatility explained

By Willem le Roux, Head: Investment Consulting, Simeka Consultants and Actuaries

Quarter 1: 2015

“Risk comes from not knowing that you’re doing.” – Warren Buffet

Trustees and members should not confuse the concept of risk with the usual investment measure of volatility. An asset with high volatility is only risky if you need to sell those assets in the short term and therefore have a high level of uncertainty of what price you will get. Rather, understanding risk requires understanding your needs as an investor.

A young member saving for retirement should pay attention to one big risk before considering any others, as it will have the most defining impact on his / her retirement. This is the risk of insufficient returns. By way of illustration, let’s say someone saves toward retirement for 40 years and then lives for 40 years as a pensioner before passing away. If no investment returns are earned on the money (and the savings don’t change in real terms), notionally this person would have to save 50% of his / her income towards retirement while working, since half of every pay cheque should go toward supporting living expenses in the first 40 years and the other half for the last 40 years. It’s simple maths. The only reason that the burden is not so heavy in reality is that investment returns are earned on savings and the effect of compound interest (informally referred to as the eighth wonder of the world) does the rest.

In the United States this has led to investment strategies for younger members that are more aggressive than Regulation 28 traditionally allowed. However, the current version of Regulation 28 permits more flexibility and allows trustees to increase the risk profile of an aggressive Regulation 28-compliant balanced investment portfolio. The additional options that they can select from (along with 75% exposure to equities) include a 15% exposure to hedge funds and private equity (10% maximum for each of these), 10% exposure to commodities and 25% exposure to property (with no maximum on the combined exposure of equity and property, meaning it could theoretically take up the entire portfolio). Furthermore, additional geographic diversification is allowed through Africa exposure of up to 5% in addition to the 25% exposure to international assets generically. Total foreign exposure can therefore reach 30%. This is not new, but the application thereof has been lagging from the asset management side. We investigate the potential benefits below.

Over the long term (40 years) the predictability of an aggressive investment strategy increases. And so there are levers that a long term retirement investor can pull in order to increase the risk of an investment, thereby making it more aggressive and hopefully achieving a better long term return.

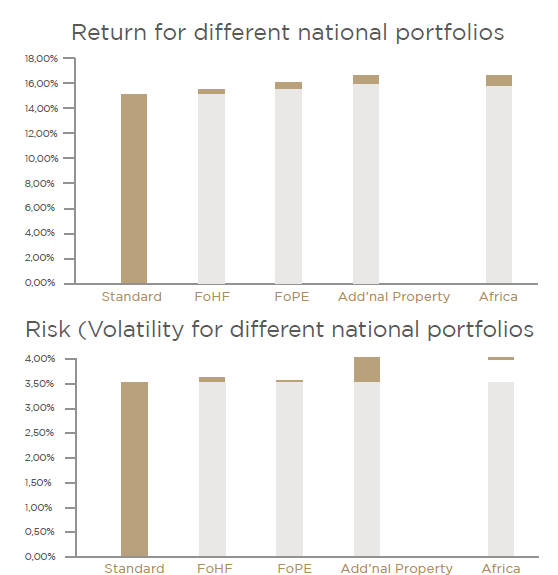

The two charts below show the impact of using these levers on the return and volatility profile of an aggressive investment portfolio.

Source: Simeka Consultants and Actuaries, 2015

The charts above show that the returns of a more typical Regulation 28 compliant portfolio could have been enhanced by more than 0.5% per year with the use of these alternative asset class allocations over the last 15 years (measured toward the end of 2014). An extra 0.5% per annum makes a massive difference in the long term. It is worth noting that the Africa allocation would have reduced the total return over this period, since this geographic collective performed very poorly over that time.

However, these phenomena move in cycles and over the next 10 years this allocation may even provide the best return of all the asset classes. The conclusion is that the long term expected return can potentially be enhanced by even more than 0.5% per annum without paying too dearly in terms of the risk taken.

An investment with more inherent investment risk is expected to provide a better return in the long term in order to incentivise investors to allocate capital to it. However, that risk can, per definition, lead to losses. Trustees and members should bear in mind that the higher expected return is by no means guaranteed – particularly over shorter time periods of up to five years.

The revised Regulation 28 allows retirement fund trustees, who understand the needs of their members, a great deal of flexibility to adjust the risk profile and increase potential returns. The power lies in the hands of those who have the nerve to invest for the long term and are not discouraged and frustrated by the shorter term objectives and potential rewards of their peers.

Disclaimer

Simeka Consultants & Actuaries (Pty) Ltd, Registration number: 1998/003048/07, is an

Authorised Financial Services Provide and a member of the Sanlam Group. This publication is intended for information purposes only and the information in it does not constitute financial advice as contemplated in terms of the Financial Advisory and Intermediary Services Act.

Although all reasonable steps have been taken to ensure the information in this document is accurate, Simeka Consultants & Actuaries will not be responsible for any loss incurred or damages suffered (whether direct, indirect, special, or consequential) to you or any third party that may be attributable, directly or indirectly, to the use of, or reliance upon, the content displayed. Please note that past performance is not necessarily an accurate indication of future performances and the performance of the fund depends on the underlying assets and variable market factors.

International investments or investments in foreign securities could be accompanied by additional risks, such as potential constraints on liquidity and the repatriation of funds, macroeconomic risk, political risk, foreign exchange risk, tax risk and settlement risk, as well as potential limitations on the availability of market information. Independent professional financial advice should always be sought before making an investment decision.

Share On:

Comments are closed.