Country Bird Holdings (CBH) – My Stock Pick

Portfolio Manager Vanessa van Vuuren discusses Country Bird Holdings

Country Bird is South Africa’s third-largest vertically integrated poultry and animal feed producer, with operations also in Zambia, Botswana, Mozambique, Namibia and Zimbabwe. Of the more than 18 million birds processed in SA per week, the company is responsible for 1.3 million birds.

What we don’t like

Their SA poultry brand, Supreme Poultry, has been struggling under the weight of the high costs of raw material (maize and soya) over the past few years, and posted a financial loss in the last financial year. A flood of competing imports mainly from South America and Europe has threatened local poultry suppliers. To curb imports, local producers have requested ministerial intervention, and while they have successfully obtained a tariff regime against South American suppliers, they have not yet obtained protection from European producers, who are allegedly dumping cheap leg quarters onto the SA market below cost of production.

What we like

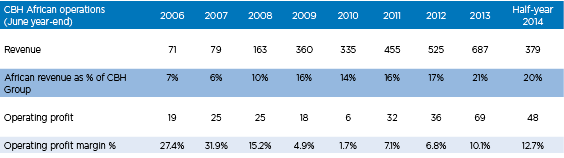

The poultry industry is very cyclical and the elevated raw material costs we’ve seen in the system will abate as US corn prices fall and local prices drop on the back of an excellent current SA maize crop. This significant relief in the cost of raw materials and the anticipated duty to be imposed on European imports bode well for Country Bird’s SA operations. The business has won contracts to supply KFC in SA and continues to successfully shift its poultry production mix to higher value and more profitable areas such as the quick-service restaurant landscape. Their African operations in Botswana and Zambia (now 20% of group revenue) have steadily been growing since inception (see table below) and display excellent growth prospects as these poultry landscapes are less developed than the SA poultry industry, offering the prospect of higher returns (at some higher risk). In Zimbabwe, it holds a master franchisee agreement to represent KFC and has started to roll out stores, with the prospect of setting up operations to supply the quick-service market in Zimbabwe as well.

Risks to the investment thesis

Firstly, maize and soya comprise 60-65% and 20-25% of chicken feed costs respectively and volatility in the prices of these raw materials could hurt the business. Secondly, there is the risk that the pending European anti-dumping duty does not materialise. Lastly, brining legislation – which limits the amount of salt water or marinade that can be injected into chickens to 15% of the chicken’s weight versus a current industry average of 25%–30% – is pending in SA. Imposing this legislation will effectively reduce the yield/volume of poultry producers on the same cost base, lowering profitability if not offset by a price increase.

The bottom line

Country Bird is at the bottom of its earning cycle and while we still expect weak results for the 30 June 2014 year-end, cyclical factors and well-performing African operations should assist the business in coming years. This should improve the company’s share price, which is currently undervalued.

Share On:

Comments are closed.