Glacier By Sanlam Launches Retirement Income Solution

Combining an income for life with an opportunity to take part in market growth

Up to now, retirees enjoyed only two options at retirement: use your capital to buy a guaranteed life annuity with no market exposure from an insurer, or invest your capital in a living annuity with no guarantee that your chosen income levels (draw-downs) will last. There was no product that guaranteed an annuity for life and provided market exposure – until Glacier launched its Investment-Linked Lifetime Income Plan.

With living annuities, many retirees struggle to decide what would be an appropriate and sustainable income in their circumstances. It they choose too high a draw-down level, they may erode their capital during their lifetime. But retirees also want the investment freedom of choosing their own investment portfolio that will keep up with and potentially exceed inflation over the long term.

Glacier’s solution combines the investment flexibility of a market-linked living annuity with the longevity protection of a guaranteed life annuity. It does this by guaranteeing retirees a fixed number of retirement income units per year, the value of which will move in line with the performance of the funds that you have chosen, under advice from your financial intermediary. So with the appropriate fund selection you can reasonably expect the value of the retirement income units to keep pace or exceed inflation, although market volatility can result in the value dropping from one year to the next.

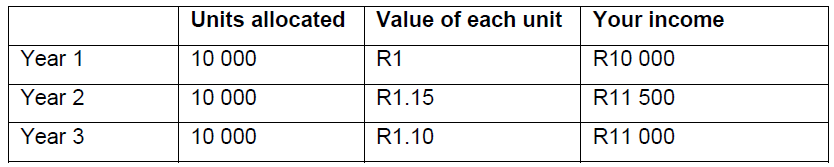

At the starting point, each of your units is valued at R1. Thereafter, units increase or decrease in value as market movements drive the value of your chosen underlying fund options (normally a unit trust fund). For example, your experience in your first three years of retirement could look like this:

Although the Investment-Linked Lifetime Income Plan is market-linked, it should not be confused with the market-linked living annuity.

How it differs from a living annuity

In essence, the capital of the living annuity is invested in the underlying funds, whereas with the Investment-Linked Lifetime Income Plan, it is the retirement income units that are invested. With a living annuity you can draw any amount between 2.5% and 17.5% of your retirement capital every year. If you draw too much you run the risk of running out of income during your lifetime. The Investment-Linked Lifetime Income Plan removes this risk but differs from a living annuity in a few important ways:

1) You do not choose your level of income

Because Sanlam carries the risk of making sure that you receive an income for life, it determines the number of retirement income units that you are guaranteed to receive. This number of units is determined at the start of the plan and is based on factors such as the amount invested, your age and gender, the length of any guaranteed payment term and whether you make provision for the income to continue for a second person. The number of guaranteed retirement income units will be lower if, for example, you choose the joint life option or if you select a longer guaranteed income payment term. The reduced number of retirement income units are your compromise for giving your dependants an income after your death. On the flipside, the number of retirement income units allocated at inception will increase if you choose an income acceleration rate. The income acceleration effectively capitalises future returns to provide a higher number of retirement income units. This means you will receive a higher income at inception, but the income acceleration rate will be offset against future growth in the value of the retirement income units.

The value of the retirement income units is adjusted annually and your income re-calculated as the number of retirement income units multiplied by the new value of each retirement income unit.

2) You cannot bequeath your retirement capital at death

When you die, there is no capital left in the product, but if you have chosen the joint life option the second life will continue to receive an income after your death for the rest of their life. Or should you die within the guaranteed income payment term, the nominated beneficiary will receive an income for the remainder of that term.

In search of a steady income

While your number of retirement income units remains fixed, the value of these units fluctuates with the market. One way to ensure a steady, minimum guaranteed income is to choose a fund with a guarantee. A guaranteed number of units means you will not run out of an income during your lifetime, but you need to choose your funds wisely to ensure your income amounts do not fluctuate at levels that you are uncomfortable with.

Always speak to a financial adviser before you make a decision around such an important event as your retirement.

Share On:

Comments are closed.