Retirement annuities: is the tax refund worth it?

When it comes to tax, government rewards taxpayers for making choices that benefit society. Donating money to approved charitable organisations is one way to get some tax back from SARS; paying family members’ medical aid contributions is another way. These expenses are purely altruistic, though, and do not contribute to your own material wealth. But there is a way to build your own investment portfolio and be rewarded with a tax refund. Contributing to a retirement annuity (RA) holds the best of both worlds: build long-term wealth and reap the tax benefits.

Why would SARS reward RA investors with a tax refund?

SARS rewards you for contributing to a retirement fund now so your older self does not become dependent on the state – or society – in retirement. Therefore, since 2016 you can contribute up to 27.5% of your total annual income to a retirement fund (the contribution is capped at R350 000) and get a tax refund. Examples of a retirement fund is a pension fund, a provident fund and an RA.

An RA has other benefits too

An RA has several benefits other than a tax refund on annual contributions: no tax on interest, dividends or capital gains while you remain invested; protection against creditors; and protection against yourself (you can’t touch the money until age 55) – to name a few. A new-generation RA also allows you to stop your contributions at any time and take it up again at a later stage. We’ve created an RA infographic to show all the main tax and other rules of an RA, such as the withdrawal limits when you retire and the deferred tax, but in this article we’ll focus only on the aspect of an RA that we receive the most questions on: how does the tax relief on contributions work?

We’ll show you with a few examples how your RA contributions can affect your annual tax bill.

Examples of how an RA provides tax relief

To keep the calculations simple and to focus solely on the tax relief offered by saving for retirement, we assume in all our examples that you had no other tax-deductible expenses. We also assume that you are younger than 65. After age 65 you enjoy higher tax rebates.

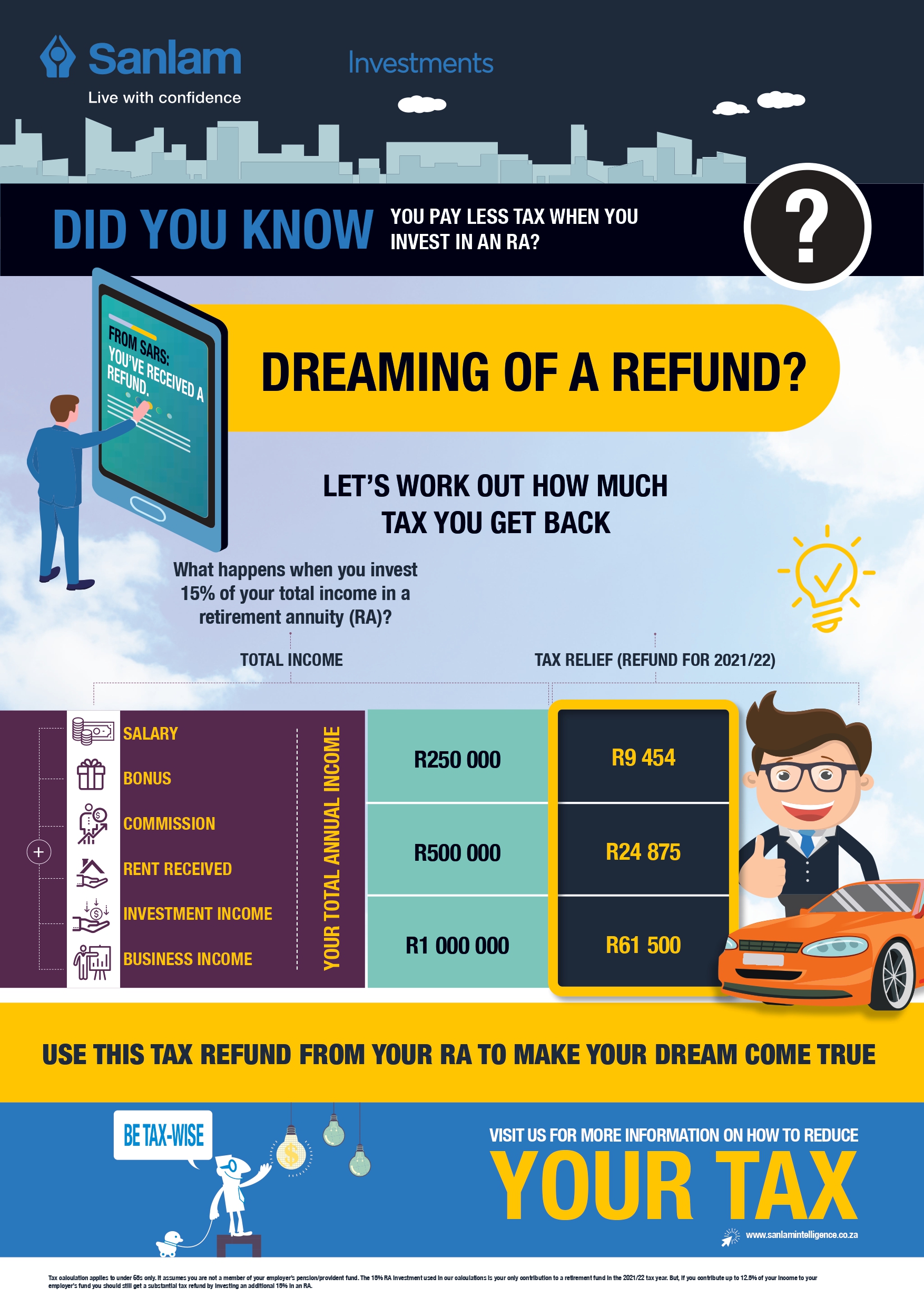

Example 1: You earn R500 000 and contribute 15% to an RA

Using the SARS tax tables and current primary rebate of R15 714, we calculate that you would have paid income tax of R106 725 if you didn’t contribute any amounts to a retirement fund. However, your 15% contribution to an RA (0.15 x 500 000 = 75 000) reduces your taxable income from R500 000 to R425 000. As a result, you need to pay income tax of only R81 850, not R106 725. This means, if you earned R500 000 during this tax year, your 15% contribution to an RA saves you R106 725 – 81 850 = R24 875 in tax!

Is an RA worthwhile if you are already contributing to your employer’s fund?

What if you’re already contributing to your employer’s pension or provident fund? Is it worth contributing to a private RA too? If you haven’t yet maxed out your 27.5% allowance, yes, you definitely want to consider an RA too.

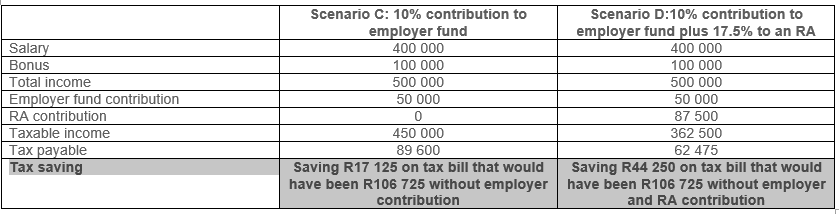

Example 2: You earn R500 000 and contribute 10% to your employer fund and 15% to an RA

If you earn R500 000 in the 2021/22 tax year and you’re already contributing 10% to your employer’s retirement fund, adding another 15% to an RA will lead to a meaningful additional tax saving.

Again, using the SARS tax tables, we calculate that you would have paid income tax of R89 600 if you contributed 10% to your employer fund only. Your additional 17.5% contribution to an RA (0.175 x 500 000 = 87 500) reduces your taxable income from R450 000 to R362 500. As a result, you need to pay income tax of only 62 475, not R89 600. This means your 17.5% contribution to an RA saves you an additional R89 600 – 62 475 = R27 125 in tax.

How you use your tax refund is up to you

How you use your tax refund is entirely up to you. Settling any debt that you may still have first is always a good idea. Or you can use it as a deposit towards your first home or to pay for your child’s education fees. Another great use of a tax refund is to invest it in a tax-free savings account, bearing in mind that the annual limit on tax-free account contributions is R36 000 per tax year.

Remember to submit your RA certificate

Keep in mind that SARS can only provide you with a refund or lower tax bill if it knows about your RA contributions. Therefore, keep your RA tax certificate in a safe place and remember to enter the total contributions for the tax year when completing your next tax return. SARS will also ask you to submit your RA tax certificate along with the rest of your supporting tax documents.

What if you don’t have an RA?

It is possible to open an account within a few days. Discuss the options with your financial planner and make sure you understand the total costs and restrictions involved, as well as the risks attached to the underlying funds in your RA.

We offer index-tracking (passive) funds for your RA

The Satrix Retirement Plan has the Satrix Balanced Index Fund and Satrix Low Equity Index Fund as underlying investment choices. More information is available on sanlaminvestments.com

Share On:

Comments are closed.